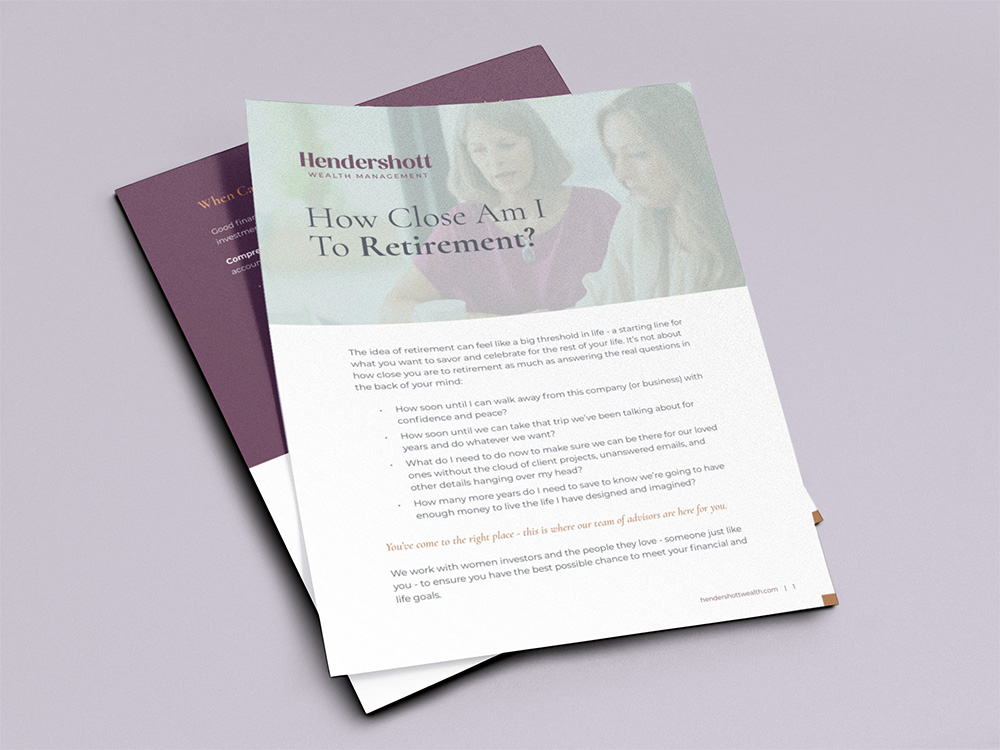

Fee-Only Fiduciary Financial Advisors & Wealth Managers

You don’t want just a wealth manager. You need a true financial partnership.

Our premium client services take care of all your comprehensive financial needs:

- Income Tax Planning

- Estate Planning

- Insurance

- Investment Portfolio Construction

- Retirement Income Generation